April 7, 2020

Crisis offers recordkeepers opportunity to stand out from the crowd

The rapid spread of corona virus has resulted in the U.S. economy coming to a screeching halt….

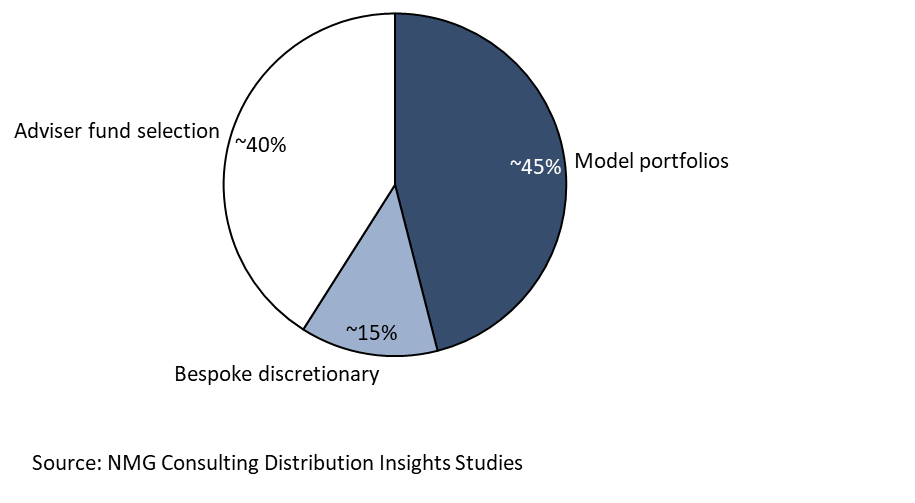

Model portfolios are an important part of the UK independent financial adviser channel, accounting for around 45% of advised client assets, with a further 15% of assets sitting within bespoke discretionary portfolios (figure 1).

Figure 1: Split of UK independent financial adviser channel AUM by investment solution

The growth of model portfolio usage has been driven by regulatory forces and changes in provider propositions:

Independent discretionary fund managers (DFMs) have evolved from private client stockbrokers to become model portfolio providers, managing ~50% of model portfolios assets in the UK (the remaining 50% being managed within models run by the advice firm, a platform or a back office technology provider). And there are plenty of strategies that independent DFMs can employ to protect and grow share-of-wallet within existing advice firm clients, including integration with financial planning software and support with business continuity.

However, as the economic shock caused by COVID-19 increases demand for model portfolios, in this Citylogue we will explore what DFMs can do to capture the new business opportunities within the financial adviser channel.

So, what do these new business opportunities look like?

The answer depends on the scale, internal capability and operating model of the advice firm:

While DFMs had success in supporting networks and national advice firms in launching their own model portfolios, only a handful of these opportunities remain. And most DFMs are willing to white-label investment solutions for only a small number of preferred investment specialist adviser clients, due to the increased costs and the risks associated with jointly-run model portfolios.

Instead, it is the general practitioners that hold the greatest opportunity for DFMs.

However, DFMs are not alone in competing to be the model portfolio provider for general practitioner advisers.

In order to successfully differentiate from a broad range of competitors, model portfolio providers must understand how they are selected by advisers.

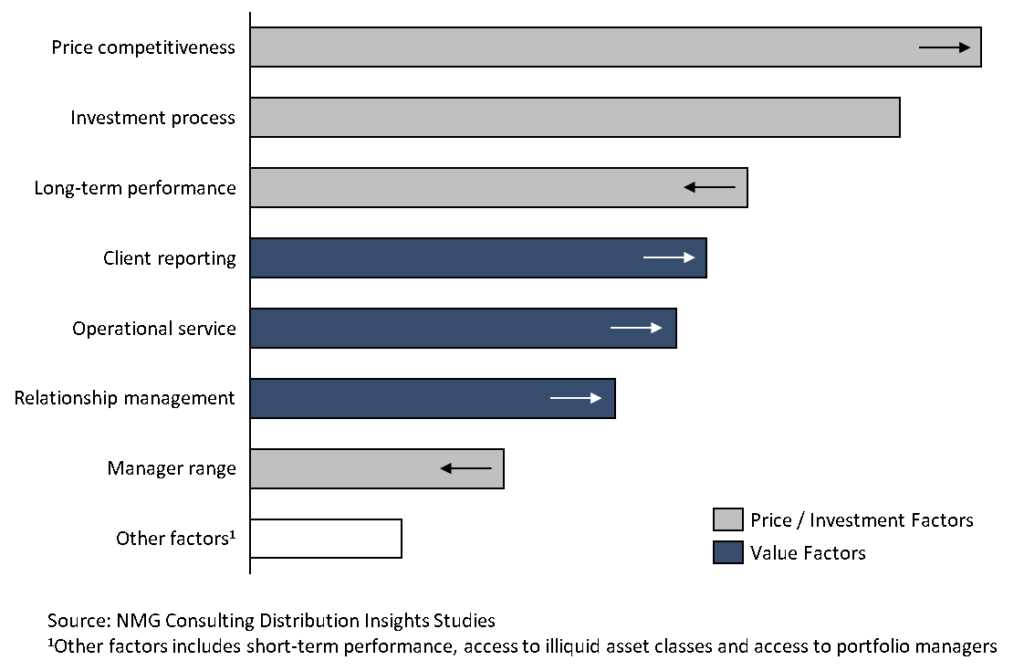

Feedback from NMG’s distribution insights studies shows that, at a high level, price is becoming more important and performance less so, but deeper analysis indicates that the solution is more complex. In fact, advisers select DFMs on how they align to their advice proposition, based on a range of value factors, including client reporting, operational service and relationship management (figure 2).

Figure 2: Top-3 factors for selecting DFMs (by general practitioner advisers)

If this sounds familiar, it should – as DFMs play an increasingly important role in both the back and front office functions of advice businesses, they will take on product wrapper provider-like responsibilities and, in turn, will be selected by advisers on this basis. Successful DFMs will position themselves more competitively by understanding the changes to the process by which they are selected and shaping distribution and M&A strategy accordingly.

So, it is clear that there is no singular winning solution for DFMs. Instead, successful strategies will be targeted at specific financial adviser subsegments and their relevant model portfolio provider selection factors, including:

At NMG, we are working with DFMs to optimise their existing client base, define their distribution strategy and identify M&A opportunities to build competitiveness. For more information, contact:

Charles Lake, Principal Consultant (London; [email protected])

Rodolfo Crespo, Senior Consultant (London; [email protected]