July 17, 2024

Understanding DC Advisors’ preferences

Recordkeepers face a complex challenge in addressing both the explicit and implicit preferences of DC Advisors. Advisors...

Many retirement plan advisors expect revenue growth but face rising costs and continued fee pressure. In today’s market, success is no longer defined by growth alone. Firms that strengthen efficiency, refine their value proposition and deepen client relationships are better positioned to perform in a margin-constrained environment.

Many advisors have learned, sometimes the hard way, that not all growth is good growth. Larger plans can look attractive, but they often come with tighter pricing, higher service expectations and more operational complexity. Without the right team structure and systems in place, those relationships can consume disproportionate resources and deliver less profit than expected.

Smaller plans, by contrast, are often more predictable and easier to service from a margin standpoint. That does not make large plans a bad strategy; it just makes them a different one, with tradeoffs that need to be understood up front.

As a result, advisors are becoming more selective. Before taking on new business, they are asking tougher questions: What will this relationship require from our team? Can we service it efficiently? And does it align with how we want to run our practice?

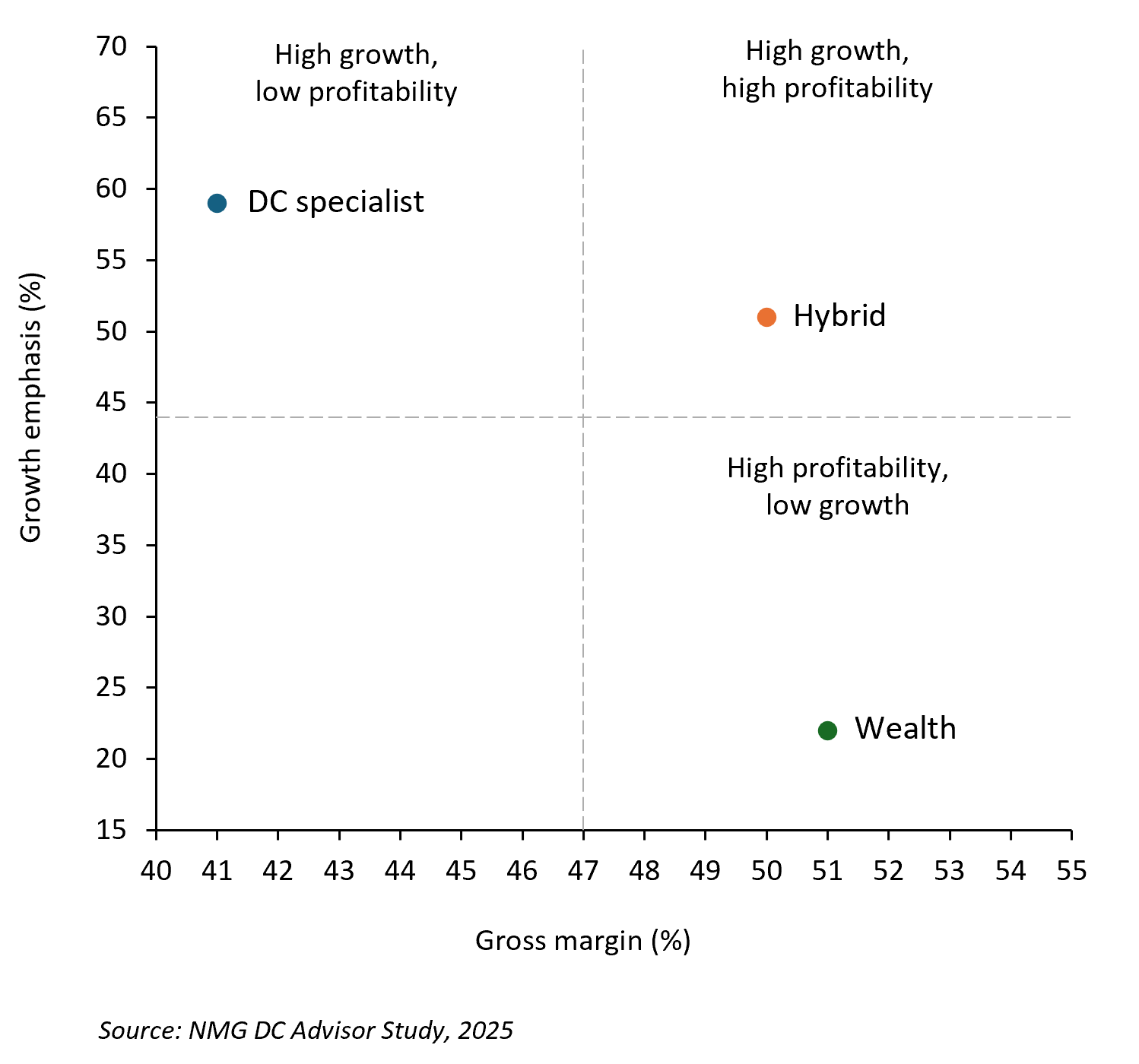

How firms experience margin pressure and respond to it varies significantly by the practice models identified by NMG.

DC specialist advisors feel the squeeze most directly. Retirement plans account for an average of 83% of their total practice revenue, which means growth is often necessary just to offset rising costs. These firms are scaling through volume, but with greater intention. Standardized service models, tighter workflows, larger teams and meaningful technology investments are no longer optional. For DC specialists, efficiency is the difference between sustainable growth and stalled profitability.

Wealth-focused advisors face a different equation. Roughly two-thirds of their revenue comes from wealth management and financial planning, with less than 20% tied to retirement plans. Given the higher margins in planning, insurance and investment management, many are less motivated to aggressively expand their DC business when it adds complexity without a clear economic payoff. Their growth strategies tend to emphasize deeper relationships, expanded services, and multi-generational wealth rather than increasing plan count.

Hybrid practices may be best positioned in the current environment. With revenue typically split evenly between retirement, wealth management and financial planning services, these firms can use employer plans as an entry point to individual relationships, capturing higher-margin opportunities outside the plan. That balance allows hybrids to grow on multiple fronts while spreading margin pressure across the business.

Exhibit 1: Growth intensity and margin profile by advisor practice model

Hybrid DC practice models exhibit a more balanced growth and margin profile

Across all models, efficiency has emerged as the most reliable driver of scale. Advisors are investing heavily in technology, not just to modernize, but to fundamentally change how work gets done. Automation, integrated platforms and early applications of artificial intelligence are reducing administrative burden, improving communication and increasing advisor capacity without a one-to-one increase in headcount.

This is not about cutting staff. In many cases, firms are still adding workers but doing so more strategically. New roles are focused on specialization and improving the client experience, not just keeping up with the workload. The firms scaling most effectively are aligning people, process and technology around a clearly defined service model.

Advisors are also becoming more disciplined about innovation. Rather than adopting every new solution that hits the market, they are prioritizing offerings that scale cleanly and fit within existing workflows. Pooled employer plans, simplified plan design features and practical retirement income solutions are gaining traction because they support growth without adding friction.

The same discipline applies to partnerships. Advisors are consolidating relationships with recordkeepers and vendors, favoring fewer partners that deliver consistent service, transparent pricing and seamless integration. For recordkeepers, ease of doing business has become a meaningful competitive advantage.

In a margin-constrained world, smart growth comes down to alignment. Growth opportunities need to fit your service model, staffing strategy and tolerance for complexity. The most successful firms are not always the fastest-growing; they are the ones building businesses that can grow well.

The next phase of advisory growth will reward discipline over expansion, efficiency over excess, and strategy over scale for scale’s sake. The firms that win will not just be bigger. They will be better built.

NMG works with asset managers, wealth managers and recordkeepers to identify ways to grow their businesses profitably. To learn more, please contact Joshua Dietch or Oliver Hesketh.