May 6, 2019

The advice gap is dramatically overstated

There have been many ‘Chicken Little-esque’ predictions that the sky is falling in, that FASEA and the...

There is no doubt that there are significant shifts occurring in the advice industry: FASEA will see many advisers leave the industry (though mostly the non-productive ones), the shift in licensing model to ‘independent’ continues unabated and the overlap between accounting and financial advice continues to grow.

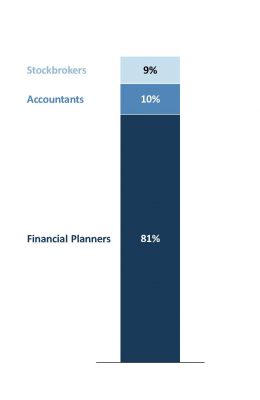

Amongst all this change, many asset managers are also considering how to engage with the almost three thousand accountants to be found on the financial adviser register.

While the sheer number of accountants might make them look like an attractive segment, we think it’s probably fool’s gold. There may be a handful of accountants who will provide investment advice on a regular basis (and therefore present a potential distribution opportunity), however, there is a different type of adviser altogether who represents lower hanging fruit for managers and platforms to consider.

Stockbrokers have been reviewing their customer proposition and advice model for some years, and are now well advanced in adopting broader portfolios, with over a third of stockbrokers’ portfolios following some centrally created and well-diversified model.

Interestingly, the last few weeks have also seen several transactions in this part of the industry (Ord Minnett, Patersons, and DJ Carmichael have all gone through ownership changes) as buyers and sellers take a different view on the ability to create value for clients in a stockbroking model. Irrespective of who is right, it is clear there is significant shift occurring in the stockbroking component of the advice channel.

As we see it, there are three shifts that make stockbroking an interesting distribution opportunity for product providers:

•Stockbrokers have always needed to move beyond Australian equities and hybrids to compete with traditional financial advisers. The breadth of listed product now available via the ASX (ETFs, LICs, LITs, bonds, etc) gives stockbrokers much better opportunities to create fully diversified portfolios, and without having to look beyond the ASX. This creates a largely new distribution market for asset managers (at least those with the right product structures).

•Brokers have historically used internal administration platforms (charged at a high cost point) to provide administration and reporting to clients. The increasingly competitive platform market will challenge stockbrokers to charge in a fashion similar to traditional financial advisers, and separate their advice and administration fees, particularly as brokers come to terms with the best interest duty.

•Brokers will be substantially impacted by upcoming advice changes – they are much less likely to meet the FASEA qualifications, and have (on average) a longer tenure than the average financial planner, which means they need to broaden their retail advice offer beyond direct equities into diversified portfolios and strategic advice to offset lost revenue.

However, as always, these things need a good catalyst for change to occur. While brokers have been thinking about the revenue model for some time given falling trading revenue, we believe the current regulatory environment will place a limit and/or timeframe on placement fees (which currently remain exempt under FOFA), forcing brokers to reconsider their proposition (not just from a revenue perspective, but also putting the client first).

Providers (asset managers, platforms and insurers) who start broadening their distribution into stockbrokers now are likely to be better placed for the opportunity presented by the slow and steady shift of stockbrokers into broader strategic advice.