September 16, 2021

MPS Market Landscape: Part 1 – Asset Managers as MPS Providers

In the first part of our MPS Market Landscape series, we will be covering - why asset...

Given growing competition from asset managers, what can DFMs do to protect and grow their share of the financial adviser channel?

In Part 1 of our MPS market landscape series, we showed how asset managers are leveraging their existing distribution, investment processes and economic model to develop MPS aligned to adviser needs.

However, the advice landscape consists of a range of IFA segments:

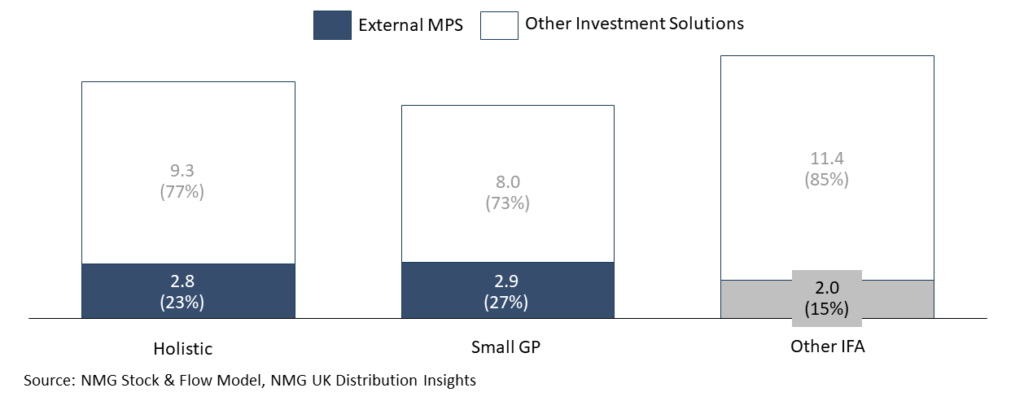

Due to the differences in advice models and underlying client needs, allocations into MPS usage are varied across these segments (Figure 1).

Exhibit 1: New flow contributions (£bn) placed by the UK independent financial adviser channel within external MPS solutions across relevant product wrappers in 2020

So naturally, this prompts the question: what does the opportunity look like for DFMs in each segment?

While some Holistic advisers have developed internal investment capability through white-labelled advisory portfolios or their own DFM permissions, many still work with external investment partners.

When selecting MPS providers, Holistic advisers cite their desire to have greater control over the investment process (customisation, white label), their customers’ requirements for greater investment complexity / asset admissibility (single stocks, unlisted assets) and their larger average client balances (with the expectation for scaled pricing discounts for individual customers).

We expect DFMs to continue to be the providers of choice for MPS in the Holistic adviser segment, given adviser and client requirements for investment flexibility.

However, in order to fully align to Holistic adviser needs, DFMs must implement targeted distribution strategies, offering a range of key account benefits to their preferred / culturally aligned advice firms, including:

Unlike Holistic advisers, price (for lower client balances) has been the primary concern for Small GPs in the design of their investment selection process. This focus on price has driven high penetration of low-cost multi-asset solutions within the segment.

However, increasingly Small GPs are citing their need for reporting and compliance efficiencies (particularly post-RDR and MiFID II) and their desire for greater transparency in the investment selection process. As such, the Small GP segment is increasingly opting to place new business into external MPS solutions (over multi-asset / multi-managed funds).

Critically for DFMs, the investment factors that drive their success in the Holistic adviser segment (breadth of investment range, access to portfolio managers, establishment of internal Investment Committee) are low priorities for Small GPs.

Instead, we expect asset managers to win in the MPS market for Small GPs because of their focus on low pricing of MPS for a range of customer balances.

Advice firm consolidation is a constraint on the Small GP opportunity for DFMs…

The biggest challenge that Small GPs face has little to do with their investment processes.

Instead, their biggest concerns are on the future ownership of their advice business as the owners and managers of the practice look to retire. This has driven the recent growth of consolidation in the Small GP segment and this presents a further challenge to DFMs in this part of the adviser market – as advice firms are bought out, assets are gradually migrated into the buyer’s own investment solutions.

…but DFMs should consider acquisition of Small GPs themselves

DFMs are natural acquirers of advice firms, with a ready supply of younger advisers looking to take on existing client books and with a unique combination of experience in both financial advice and investment management.

However, with the growing challenges in migrating client books post-acquisition, the opportunity for DFMs is unlikely to be in the acquisition of new adviser accounts. Instead, DFMs should look to their existing Small GP relationships to identify acquisition opportunities, with a view to protecting and growing share-of-wallet.

For more information, contact:

Charles Lake, Principal Consultant (London; [email protected])

Rodolfo Crespo, Senior Consultant (London; [email protected])