September 16, 2021

MPS Market Landscape: Part 1 – Asset Managers as MPS Providers

In the first part of our MPS Market Landscape series, we will be covering - why asset...

In the first edition of a series looking at the Model Portfolio Service (MPS) Market Landscape, we will discuss – why are asset managers entering the MPS market and how will they fare against Discretionary Fund Managers (DFMs)?

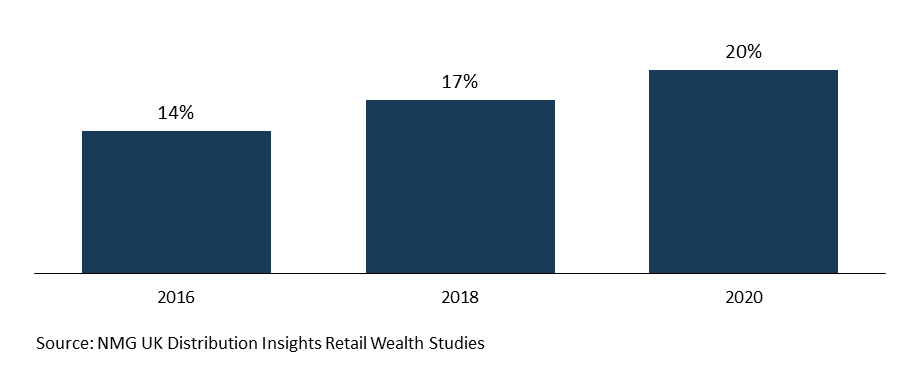

Financial advisers are continuing to increase allocations to external MPS propositions, which are the preferred investment solution for a fifth of client assets in our 2020-21 Retail Wealth Study, up from 14% in 2016 (Figure 1).

Figure 1: Percentage of new contributions placed by UK independent financial advisers in external MPS solutions over the past 12 months

This demand for outsourced investments has been driven by regulatory forces, including guidance on Centralised Investment Propositions (post-RDR) and MiFID II fee disclosure requirements, as discussed in our previous Citylogue.

DFM incumbents successfully captured the initial migration to external MPS, leveraging established investment processes and external manager relationships within their bespoke portfolio solutions to rapidly develop model portfolio services. These models then built scale through distribution relationships with adviser platforms.

However, this opportunity has largely played out:

Model portfolio management is an attractive part of the retail advisory value chain, given average operating margins of ~15bps and high asset retention (with average MPS provider relationships lasting >5 years).

Inevitably, this has attracted competition for MPS assets from other value chain participants, most recently asset managers, who are looking to expand share-of-wallet across multiple asset classes and to improve asset retention during periods of lower performance.

Several asset managers have entered the MPS market over the past 2 years, focusing on the development of the requisite investment processes (manager selection process where models are unfettered, asset allocation/risk profiling) and technology (automated reporting, portfolio rebalancing). However, this rush to enter has come at the cost of key ‘quality-of-life’ proposition components, with advisers in NMG’s annual Retail Wealth study citing the administrative burden of advisory-only models when these have been developed, limited differentiation, a lack of availability on key platforms, and overly restrictive investment ranges within some asset manager-run MPS.

So, the obvious question is: ‘can asset managers succeed in the MPS market?’

The first place to look is the MPS selection process for financial advisers.

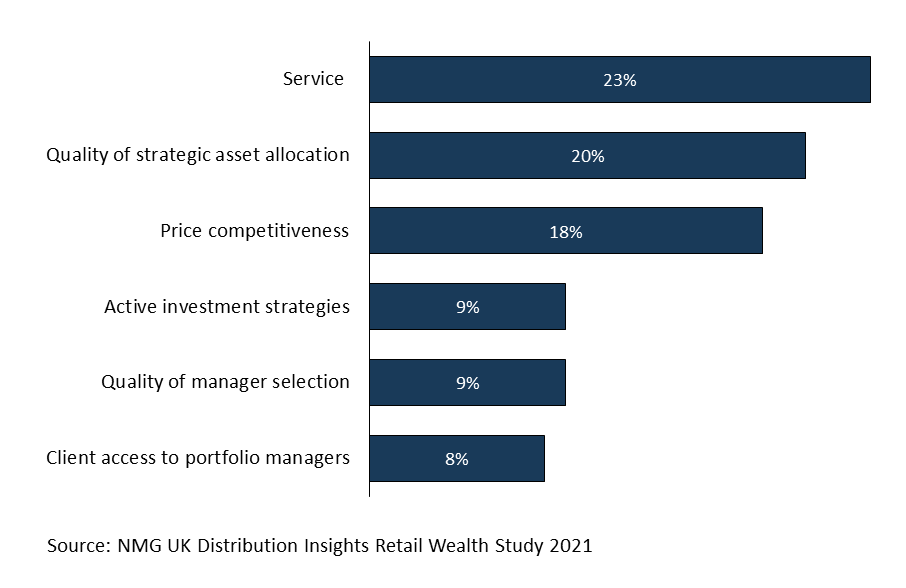

Within NMG’s Retail Wealth study, feedback indicates that a combination of high quality SAA, supported by efficient service at a competitive price, drives MPS placement (Figure 2). Critically for DFMs, the ‘quality of the manager selection process’ (once thought to be a key driver of MPS provider selection), and ‘client access to portfolio managers’ (a value-add DFMs have traditionally been happy to offer) are falling in importance.

Figure 2: Most important factor when selecting an MPS solution

When comparing the lead MPS selection factors with the propositions of asset managers, DFMs and platform/wrapper providers, it is clear that asset managers are well positioned.

Asset managers can leverage:

While DFMs have been the main benefactors of the rush to external MPS solutions, the landscape is becoming increasingly competitive, with asset managers well placed to win over advisers. So how can DFMs respond, and which market segments align best with the different propositions? We will explore this in the second part of this series.

For more information, contact:

Charles Lake, Principal Consultant (London; [email protected])

Rodolfo Crespo, Senior Consultant (London; [email protected]m)

Jake de Uphaugh, Consultant (London; [email protected])