March 13, 2023

Advice: Back to a better future

The recommendations of the Quality of Advice Review would force large institutions back to the table on...

Australia’s latent demand for financial advice is worth over A$2.2bn annually. Meeting this demand would have a profound impact on the lives of millions of Australians but requires bold policy resets.

Australia’s advice gap has expanded in recent years, as over-regulation and institutional exists have seen active adviser numbers fall ~30% from their peak, to ~11.5K1. The result is that only 10% of Australian households currently have access to financial advice.

As we’ve previously discussed, the Quality of Advice Review (QAR) was commissioned to assess ways to bridge this gap; and the 22 recommendations made in the review could be transformative for the advice landscape in Australia.

However, the Government’s current position on the implementation of QAR limits the potential benefits to Australians by focusing solely on retirement and pre-retirement advice needs.

The need for quality financial advice, or guidance, exists far beyond retirement and pre-retirement years. Whilst retirement advice can maximise the quality of life that each person’s retirement savings can provide, it is the advice received in the decades leading up to retirement that has the greater impact on quality of life in retirement.

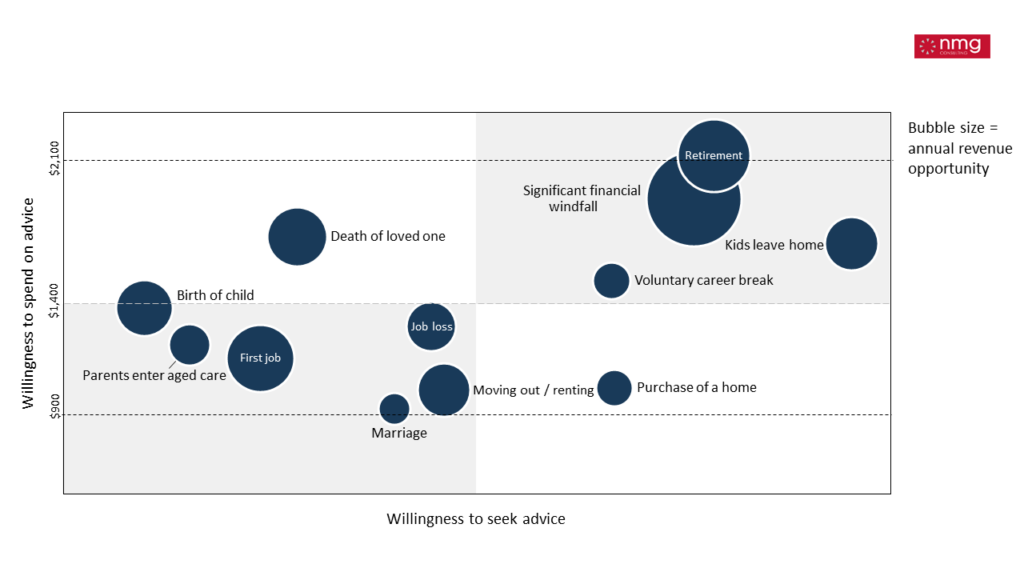

Exhibit 1: Demand for advice against willingness to pay for advice at key life events

Source: NMG Australian Consumer Study 2023

NMG’s recent Consumer Study collected responses from over 2,000 Australians, seeking to size the demand financial advice throughout a person’s life by focusing on key life events where advice could be beneficial.

It was unsurprising to see that in addition to retirement, the life events with the most obvious cashflow consequences; “dealing with an inheritance” and “becoming empty nesters”, are the events where advice is seen to be the most valuable.

However, we also saw a high desire for guidance through navigating a “voluntary career break” and “purchasing a home”. And whilst seen to be a less likely trigger to seek financial advice, those who would seek support around the “death of a loved one”, placed a high willingness to spend on that advice.

Overlaying the propensity of Australians to experience these events results in demand for over 1.7m advice events each year – 1.6m of which are not currently in scope for the Government’s implementation of QAR.

Our analysis shows that the total value of the current advice gap, considering willingness to pay for and seek advice around each life event, is $2.2bn annually. That amounts to a 45% uplift to the existing advice revenue pool in Australia.

We also see significant upside to these estimates through better education and engagement models, increasing the propensity of Australians to seek advice around key life events.

There is clearly a desire and need for advice beyond planning for retirement in Australia. The continued constraint on supply of financial advisers means this demand cannot be met via the traditional channels.

Regulatory settings permitting, we see several ways that innovative providers could step up to fill this advice gap and access the commercial opportunities it offers.

Firstly, super funds are well placed to provide financial guidance beyond retirement. They have access to significant member data with which to identify the types of life events which require advice. They have the member access and trust required to act on the information. And they have existing fiduciary obligations to govern these interactions.

Secondly, existing advice groups have the potential to tap into the “good advice” model proposed by the QAR, by partnering with super funds. This could provide advice firms with a new revenue line, acting on behalf of super trustees to provide good advice to the fund’s members, and also provide a (profitable) pathway for hiring and developing new advisers.

And as we’ve discussed previously, should the Government accept the QAR’s recommendation to open-up the provision of “good advice” more broadly, we see significant opportunities for banks and other large financial institutions.