July 11, 2025

The engagement cliff in pensions decumulation

Industry efforts around pensions engagement focus almost exclusively on before- and at-retirement decisions. With pension drawdown requiring...

The FCA’s Pure Protection Market Study raises serious questions for a market that appears to perform well by international standards. How might the regulator’s goals conflict, and in what ways could these impact key distribution models and have possibly unintended (and unwanted) consequences?

The FCA’s Pure Protection Market Study is tackling some of the most fundamental aspects of the UK protection landscape, covering themes such as intermediary incentivisation, consumer understanding and market access.

Our assessment of the potential implications, informed by our consulting experience in comparable markets globally, is that it could prove profoundly consequential for the future health of the UK protection market.

We have identified two primary concerns which will be explored in more detail below:

The Study should begin with an understanding of the current market state and whether there is a clear problem warranting regulatory intervention:

Given the absence of material concerns on key metrics, this raises an important question: what specific problem is the FCA aiming to address?

Globally, protection business placement is dominated by intermediaries, who are indispensable to the sector’s growth and accessibility.

Importantly, the type of intermediary matters. In the UK, new sales are heavily concentrated amongst the distinctly non-traditional ‘Streamlined Specialist’ segment (high-volume distributors using digitally-enabled, remote-first and operationally efficient business models to target predominantly mass-market consumers), alongside a strong reliance on Mortgage Brokers/Networks and Generalist/Investment Networks.

Exhibit 1: Contestable intermediated channel dominates UK market

New business premiums channel and segment breakdown (% APE, 2024)

The dominating distribution channels are highly effective at driving volume, but are particularly exposed to regulatory change, especially in areas like incentivisation or increased process friction. These business models typically rely on scale to compensate for thinner margins, making them heavily dependent on operational efficiency to remain commercially viable.

There is a real risk that the Study could unintentionally disrupt these critical models, potentially damaging the wider protection landscape. Crucially, these models disproportionately support lower-income customers. If they were to be squeezed out of the market, these would be the customers most affected, potentially widening the protection gap.

Some may argue that if intermediary avenues are curtailed, consumers will simply ‘find a way’ to purchase protection directly, however this view overlooks a key behavioural truth: protection policies are typically ‘placed’ (sold) and not purchased. While many consumers express a clear intention to buy, completion often relies on insurer-funded marketing and intermediary engagement that actively facilitates and completes the sale.

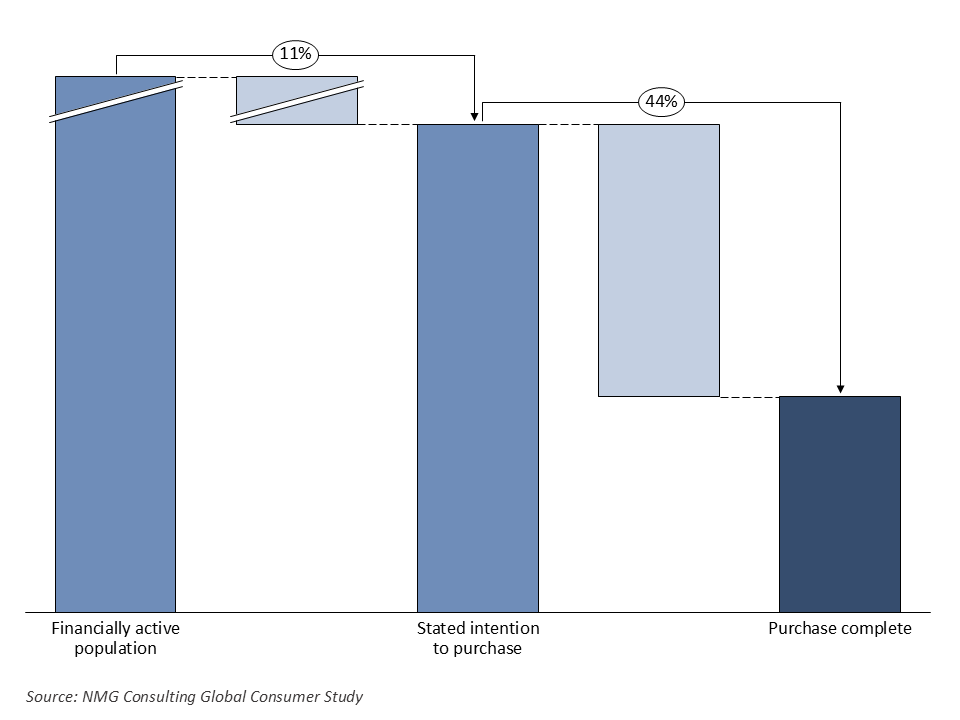

This pattern is not unique to the UK. NMG’s global research across peer life markets consistently finds drop-off rates of over 50% between stated intentions and actual purchase, with intermediaries often driving the conversion for consumers to purchase protection. In many cases, consumers may not even recognise their protection needs without the advice/guidance from an intermediary, reinforcing the role intermediaries play not just in completing the sale, but creating awareness in the first place.

Exhibit 2: Low conversion to completed protection purchase

Average drop-off rates in comparable peer markets from financially active population to stated intention to purchase protection to completed purchase

Access to protection (whether through an intermediary or otherwise) is one of the consumer outcomes that the FCA has stated they hope to achieve through the Study. Other stated outcomes include:

The FCA’s ambitions are commendable and their focus on long-term consumer outcomes is positive. There is nevertheless an emerging contradiction at the heart of the FCA’s ambitions: the desire to enhance market accessibility whilst simultaneously improving ‘value for money’, noting that it is not yet clear how the FCA will be assessing the latter.

Whilst both goals are crucial, they can conflict. For example, regulatory interventions such as commission caps, though aimed at enhancing value, may undermine the economics of servicing customers with lower premiums, potentially reducing access for those most in need of protection.

It is encouraging that the FCA has been in fact-finding mode in recent months, broadening its understanding of the intricacies of the operation of the protection market (evidenced by the acknowledgement of the role of reinsurers, portals, product comparison platforms, and lead generators on consumer outcomes in the updated Terms of Reference).

It remains unclear however whether the full consequences of regulatory action, particularly on distributor business models, is fully appreciated. The review risks disproportionately impacting Streamlined Specialists, Nationals, and Networks, causing disruption across insurer distribution channels and reducing consumer access.

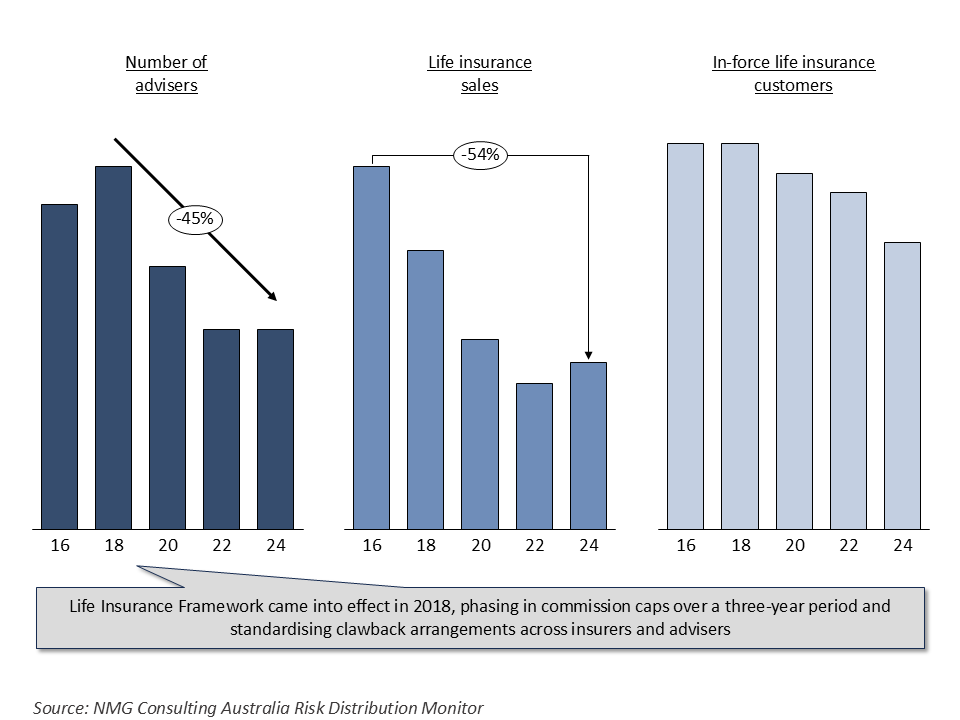

Australia offers a cautionary tale: post-2018 reforms under the Life Insurance Framework (LIF), concerned about the impact of ‘churn’ on customer value, introduced phased commission caps and standardised clawback arrangements. The result was a dramatic decline in new business volumes (down 54% in 5 years) and adviser numbers writing protection, alongside no observed improvement in persistency.

Exhibit 3: The Australian protection landscape

Number of advisers, life insurance sales and in-force insurance customers (2016-2024)

We remain hopeful that the UK market can avoid similar missteps. This position may however prove to be optimistic unless the industry engages thoughtfully with the review process.

We are hoping to contribute to the conversation by posing questions:

For the FCA:

For insurers and distributors:

If you would like to explore NMG’s perspective on the market review, or understand how it may impact your business, please get in touch with Evan Baars, Ralph O’Brien or Emma Morris.