January 21, 2025

Bridging the pensions expectation gap

How are current support services for pensions under-delivering on what consumers really want and expect – and...

Industry efforts around pensions engagement focus almost exclusively on before- and at-retirement decisions. With pension drawdown requiring decision-making long after the first withdrawal, how can pension providers deliver ongoing support throughout retirement?

In a bid to improve pensions adequacy and subsequent outcomes, great efforts have been made by the pensions industry to lift customer engagement. Once in pension drawdown, these activities taper off: it is a model built around the assumption that engagement duties largely end at the point of access. It is also a model that is now outdated.

The post-Pension Freedoms popularity of non-advised income drawdown means an increasing share of retirees now face complex, ongoing financial choices through retirement. Unfortunately, securing a sustainable income for an uncertain lifetime from a finite retirement pot is not a simple, one-off calculation. In contrast to the straightforward salary replacement of annuitisation, income drawdown’s flexibility creates new responsibilities, including investment choices, the sequencing and size of withdrawals, and tax planning. The product construct assumes continued reassessment beyond the ‘at retirement’ choice, up until the moment of pot depletion, annuitisation, or death.

FCA data shows that financial advice is flatlining, and worse, at-retirement advice is on the retreat, having fallen 6% over the past 5 years. Increasingly, consumers manage their own pension savings throughout retirement, along with the inherent risks.

Good drawdown outcomes depend on regular assessment of circumstances, but NMG’s retirement studies suggest worryingly few consumers take this approach. Instead, decumulators risk making sub-optimal decisions of import, or avoid them entirely.

As part of its focus on good customer outcomes, the FCA requires firms to:

‘Focus on the outcomes customers get, and act in a way that reflects how consumers actually behave and transact in the real world, better enabling them to access and assess relevant information, and to act to pursue their financial objectives.’

Consumer Duty, 4.8

The key phrase here is ‘in a way that reflects how consumers actually behave and transact in the real world ‘. It means that providers need to understand the hurdles that make pension decisions so counter-intuitive for consumers.

The difficulties in accumulation are well-understood: from behavioural biases to practical hurdles such as low pension literacy, affordability, and poor faith in the pension system, pension savers face a myriad of barriers to engagement.

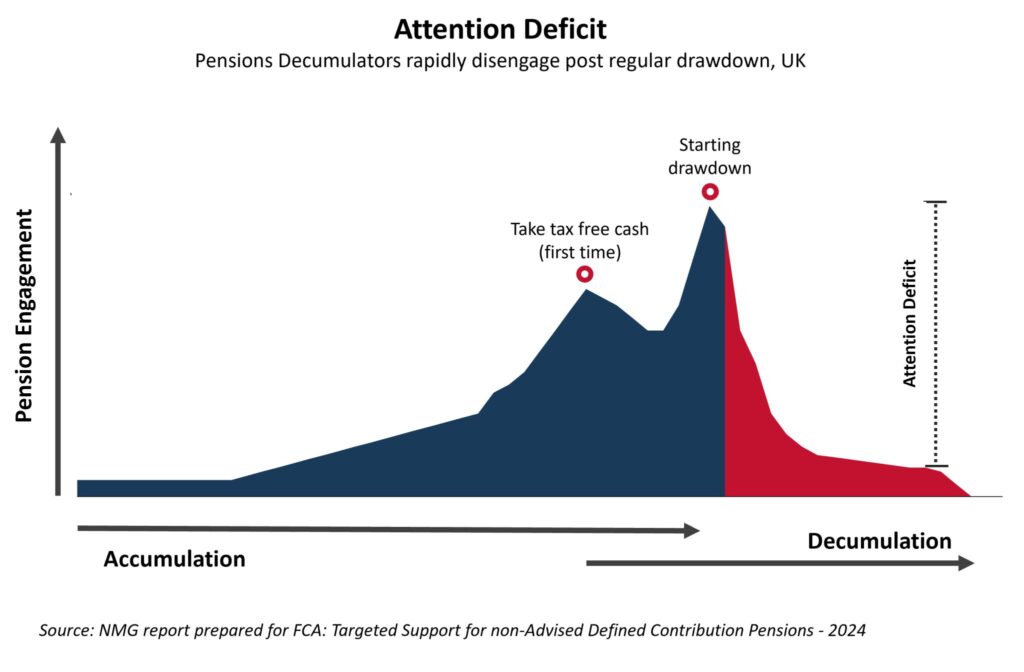

These evolve in the run-up to retirement, as pensions and their benefits become more tangible. Engagement and interest spike when consumers first take their tax-free cash or set up their drawdown policy. These moments prompt time-limited, proactive research, a necessity for the complex decision ahead.

But once in retirement, this proactive attitude falters. Recent research by NMG Consulting for Invesco showed that once pension drawdown had started, just 29% of non-advised DC retirees considered the ongoing management needed. Instead, many become closed to re-evaluating their options, finding further deliberation unwarranted or undesirable, a process known as ‘decision closure’.

While this may protect them from regret or fear, it also means pension engagement is hardest in the period when active, considered management is most important. Few consider their pension as an ongoing investment product; they assume it operates like an annuity or defined benefit pension.

Exhibit 1: Attention Deficit

Overcoming these psychological barriers to engagement is not easy; traditional methods like annual statements have limited emotional cut-through. Furthermore, many methods for engagement used for accumulators, like apps, emails, and other digital experiences, may cause problems for older customers. Digital confidence, visual and hearing difficulties, cognitive decline, and other types of vulnerability all complicate effective engagement.

All the while, the urgency to get it right is increasing. Not only are more consumers retiring with income drawdown each year, but the first non-advised cohort after Pension Freedoms is growing older and increasingly at risk of cognitive decline.

The good news is that there is plenty of white space for new propositions, fresh communications, default solutions and more, particularly with the arrival of Targeted Support. These will help customers through the entire drawdown journey, not just at the point of retirement.

Incoming legislative change is likely to drive further change. The Government has made it clear that providers have a duty of care to customers not just at, but through retirement:

‘A pension, and a pension provider’s job, isn’t done once a saver enters retirement. Instead the task is to support them through as comfortable as possible a retirement.’

Torsten Bell, UK Pensions Minister,

Workplace pensions: a roadmap June 2025

This gives huge opportunity for the pensions industry. Solutions need to be designed for the way decumulators actually engage with their pension if they are to lead to good outcomes. Providers need to understand the what, why, how and when of their decumulation customers to successfully build journeys, guardrails, and products that fit these behaviours.

NMG is working with pensions providers to investigate these issues and potential solutions. Please contact Jane Craig or Miba Stierman if you would like to know more.