July 17, 2025

FCA Pure Protection Market Study: are value and access already in balance?

The FCA’s Pure Protection Market Study raises serious questions for a market that appears to perform well...

The FCA’s interim findings stop short of structural reform — and that matters. While transparency and value metrics will face greater scrutiny, the report does not identify systemic harm in distribution. Instead, it reflects a simple reality: expanding protection requires strengthening the channels that deliver it.

The Pure Protection Market Study was launched to test whether distribution practices, intermediary incentives and product design are delivering good consumer outcomes. It examined value for money, switching behaviour, panel dynamics and whether the market structure supports access and competition.

The interim report provides a structured diagnosis of these issues. Crucially, it does not conclude that the distribution model is fundamentally flawed.

Ahead of the report, NMG argued that the market treads a fine line between value and access. The interim findings broadly reinforce that framing. The question now is not whether change is required, but how to ensure reform strengthens, rather than weakens, the primary lever for closing the protection gap: effective distribution.

The interim report is best read as diagnostic rather than prescriptive. It highlights themes familiar to market participants:

Importantly, the report does not conclude that the distribution model is fundamentally flawed, nor does it present compelling evidence of systemic detriment driven purely by incentives. Instead, it raises legitimate questions about transparency, consistency and evidencing of value.

As the FCA moves towards its final report, attention is likely to focus on value metrics, claims performance, persistency, switching behaviour, and panel dynamics. These issues matter but must be assessed alongside their impact on access.

The existence, and persistence, of a large protection gap is not in dispute. What matters is how that gap is interpreted.

Viewed through a needs-based lens, unmet demand concentrates around two core risks: income replacement during incapacity and financial resilience for dependants or liabilities. The scale of under-protection is stark.

However, the key insight lies in why needs remain unmet. While product design, underwriting constraints and genuine affordability barriers affect some consumers, they are not the dominant explanation. Behavioural and structural drivers are more powerful: low engagement, inertia, limited understanding and (critically) access to intermediaries willing and able to prioritise protection conversations.

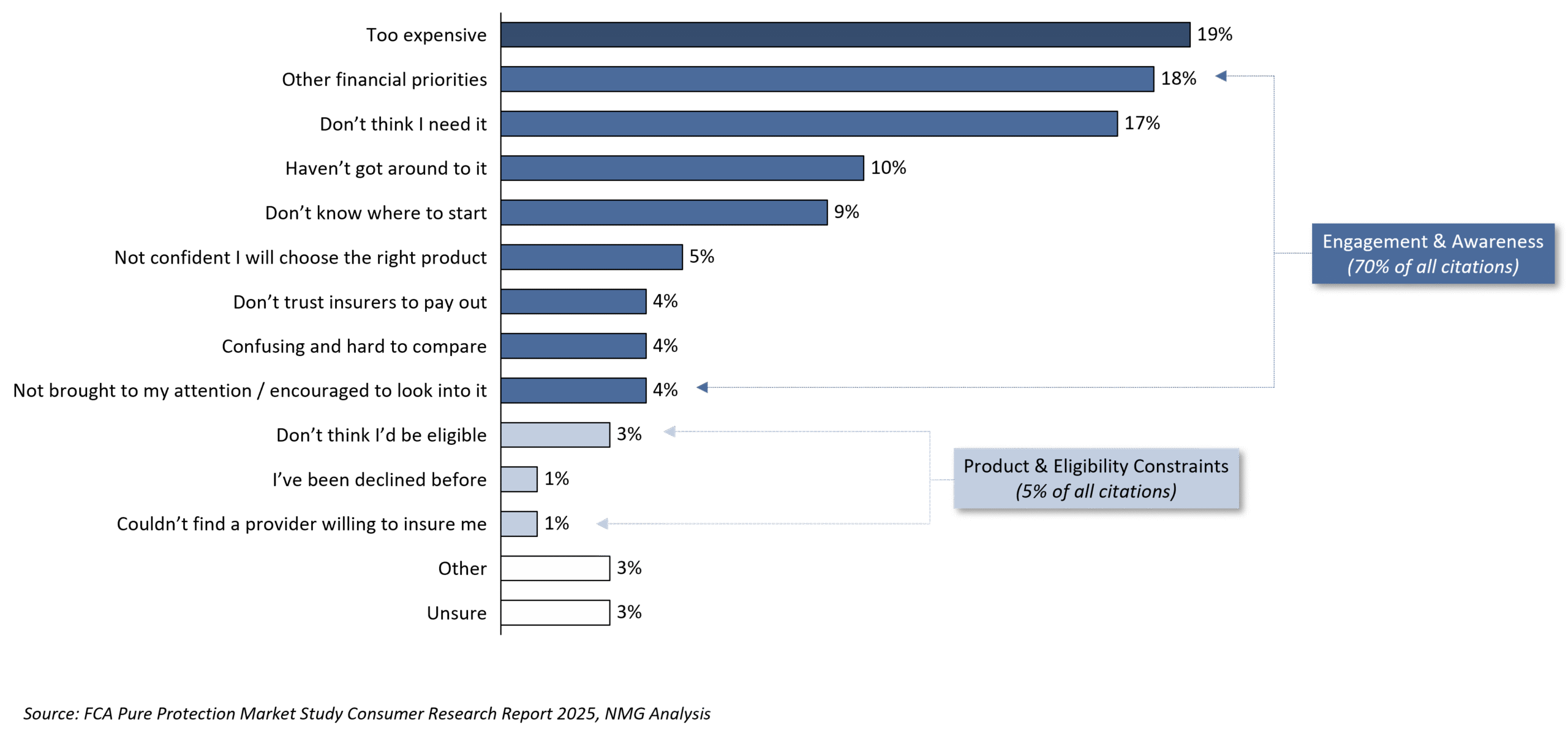

The FCA’s own research reinforces this point: the primary barrier is not product availability, but low salience and lack of engagement.

Exhibit 1: An engagement challenge, not a product constraint

Primary reason for not owning a pure protection product

If under-protection is primarily an access and engagement issue, reforms that reduce adviser participation or add material friction risk widening the gap rather than narrowing it.

Distribution sits at the centre of the review for good reason. Intermediaries translate abstract protection needs into real-world cover, particularly for consumers unlikely to self-initiate a purchase.

Adviser incentives, commercial models and process requirements shape how much time and resources can be devoted to protection, especially for lower-premium or less financially engaged households. Evidence consistently shows that when adviser economics are materially weakened or friction significantly increased, placement activity falls. Those most affected are rarely affluent or highly motivated consumers, but those already on the margins of engagement.

The UK’s large-scale and mortgage-adjacent distribution models have expanded reach, but operate on finely balanced economics. Small changes to incentives or reporting requirements can have outsized effects.

The more constructive question, therefore, is not simply what the FCA should avoid, but what it should actively do to support closing the protection gap. If distribution is the lever, policy should focus on reducing unnecessary friction, improving comparability and disclosure, supporting innovation in hybrid advice models, and enabling scalable approaches such as targeted support.

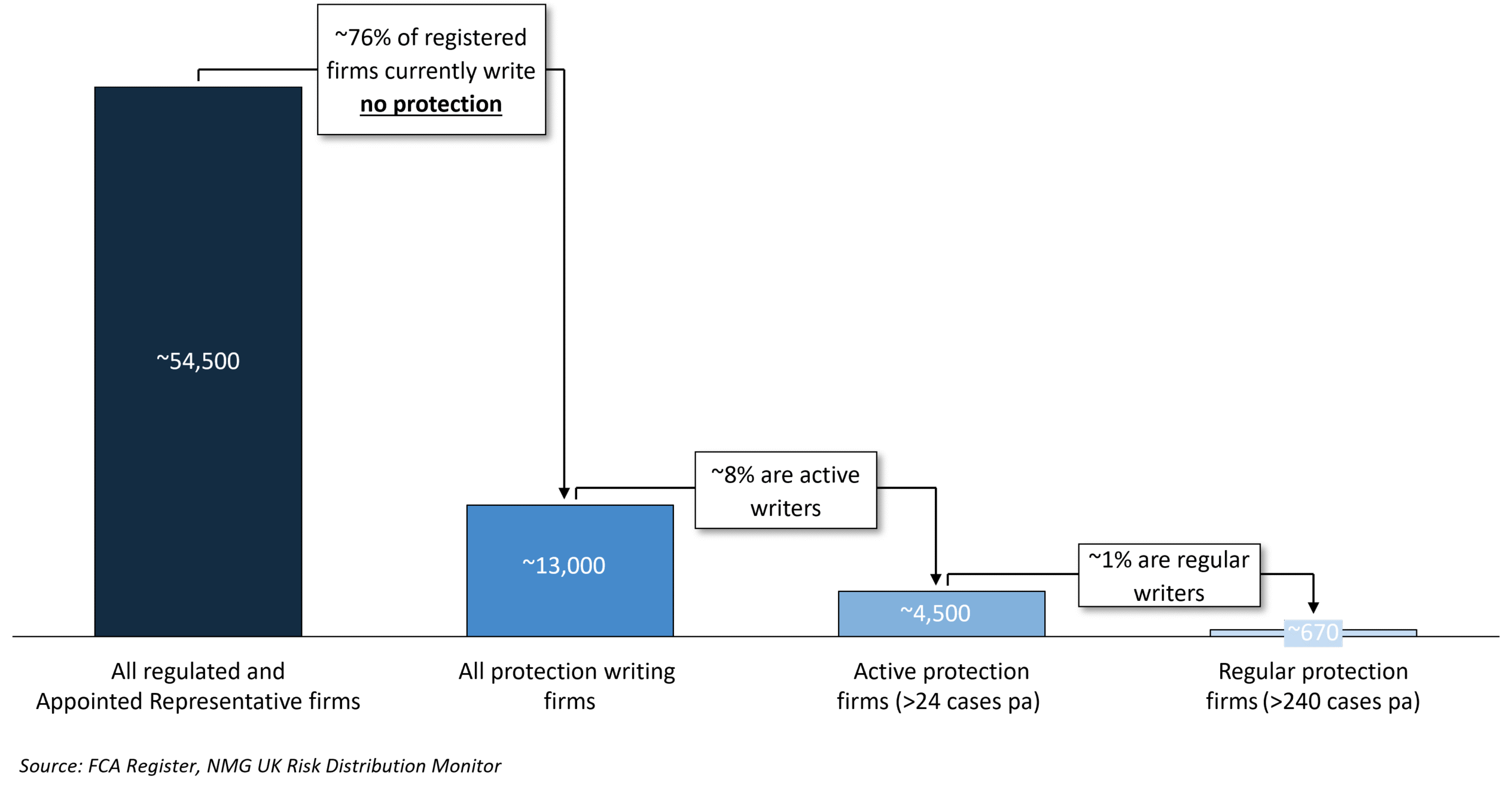

Exhibit 2: Protection written by the few, not the many

Number of protection-writing intermediaries

The FCA’s emphasis on fair value is both expected and appropriate. Ensuring outcomes proportionate to cost is central to the Consumer Duty.

However, value in protection is not solely a function of price or headline claims ratios. It is shaped by suitability, coverage alignment, underwriting quality and, crucially, whether a consumer reaches the point of being protected at all. A product that is theoretically good value but never purchased does not improve resilience.

While the FCA has generally adopted a principles-based approach in previous value-for-money reviews, evidencing requirements must remain proportionate. If they become overly standardised or process-heavy, they could unintentionally favour simpler, commoditised propositions and make it harder to justify differentiated or innovative solutions, particularly in areas such as income protection where claims experience and product design vary materially.

Metrics such as claims acceptance rates and persistency are useful and accessible indicators of value, and greater transparency would be constructive. They should, however, be interpreted in context: taking account of underwriting mix, target market and distribution channel to avoid reductive comparisons.

Similarly, questions around loaded premiums sit within the transparency debate. Greater clarity for consumers may be appropriate, but intervention should focus on improving understanding rather than undermining commercially viable distribution models serving mass-market clients.

The findings align closely with the FCA’s developing targeted support framework. Pure protection is well suited to scalable, guided support: needs are widespread and relatively well defined, yet frequently unmet due to inertia rather than rejection.

Reducing the protection gap will require lower-cost, scalable forms of support alongside full advice. Targeted support represents one of the most credible routes to expanding protection coverage at scale, provided it complements rather than competes with advice-led models.

As the FCA moves towards its final report, the central question remains: will any of the proposed changes result in more people being meaningfully protected?

Improving value for those already well served matters. But closing the protection gap requires sustaining, and where possible enhancing, the ecosystem that drives reach.

The interim findings do not justify wholesale restructuring of distribution. The opportunity now is to refine transparency, strengthen trust and unlock scalable access while reinforcing the mechanisms required to close the gap.

If you would like to explore NMG’s perspective on the market review, or understand how it may impact your business, please get in touch with Evan Baars, Ralph O’Brien or Emma Morris.